India’s electricity demand is witnessing a rapid surge, nearly doubling every decade, fueled by a strong economic growth.

Dramatic cost reductions over the last decade for wind, solar, and battery storage technologies position India to leapfrog to a more flexible, robust, and sustainable power system for delivering affordable and reliable power to serve the growing power needs. India has also set ambitious clean energy targets – aiming to install at least 500 GW of non-fossil based power generation capacity by 2030. Additionally, Renewable Purchase Obligations (RPOs) at the national and state levels require electric utilities to source at least 43% of their energy from renewable sources, including large hydro by 2030. As India’s grid attains higher penetrations of renewables, balancing generation variability through a spectrum of flexible resources, particularly energy storage, becomes increasingly important for ensuring the affordability, stability, and reliability of grid power. India has already set a national target for energy storage, aiming to meet 4% of its electricity demand by 2030, which translates to approximately 200-250 GWh of grid-scale storage capacity.

In this context, the dramatic decline in energy storage costs—marked by a nearly 90% reduction in global storage prices over the last decade and recent energy storage auctions in India reflecting a 65% cost reduction since 2021—could be a pivotal moment. This cost reduction enables the cost-effective supply of low-cost renewable electricity during peak demand periods, addressing key limitations of RE. Furthermore, with a substantial portion of India’s electricity grid infrastructure yet to be built, these cost declines present a unique opportunity for India to leapfrog to a more flexible, resilient, and sustainable power system, positioning it as a global leader in clean energy innovation.

The objective of this study is to assess:

The study uses the latest RE and storage cost data, an industry-standard power system modeling platform (PLEXOS), and exhaustive analytical methods (optimal capacity expansion and power plant-level hourly grid dispatch simulations).

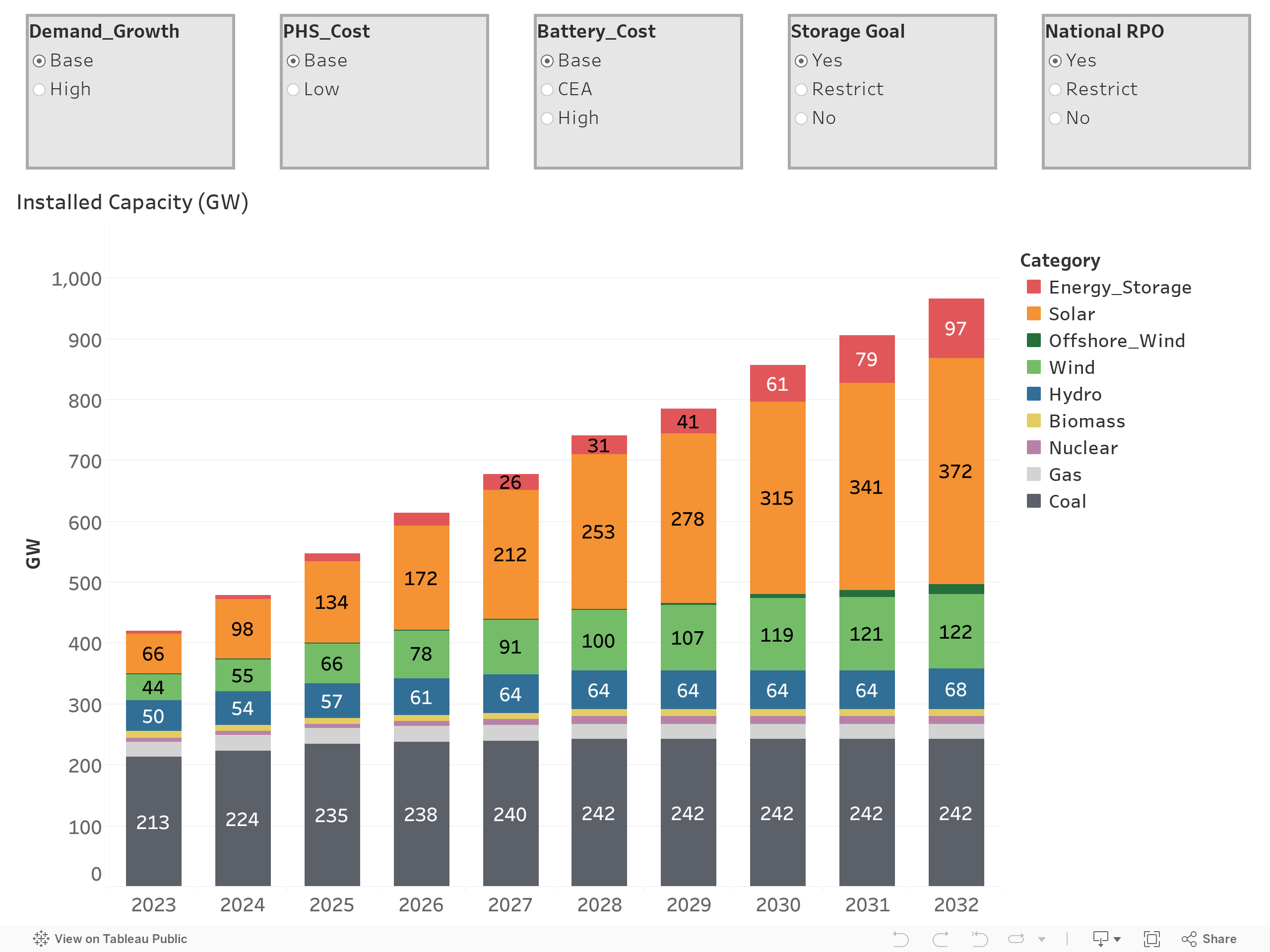

In the “Reference Case” scenario, which assumes utilities comply with the current state and national Renewable Purchase Obligations (RPO) and energy storage targets, India’s total non-fossil capacity is projected to exceed 500 GW by 2030 and reach approximately 600 GW by 2032 (as shown in Figure 1). By 2030, a total renewable energy capacity (excluding large hydro) of 456 GW is identified as cost-effective, comprising 315 GW of solar, 119 GW of onshore wind, 7 GW of offshore wind, and 15 GW from small hydro and biomass. By 2032, this renewable energy capacity is expected to grow to 524 GW, with solar accounting for 372 GW, onshore wind for 122 GW, offshore wind for 15 GW, and small hydro and biomass contributing 15 GW.

Figure 1. Installed Capacity in the “Reference Case” scenario that assumes utilities comply with the current state and national Renewable Purchase Obligations (RPO) and energy storage targets

By FY 2030, approximately 61 GW / 218 GWh of energy storage is found to be cost-effective to support renewable energy (RE) deployment, aligning with India’s national storage targets. As electricity demand and RE capacity expand, this storage requirement is expected to grow to 96 GW / 362 GWh by FY 2032. This represents substantial growth from India’s current energy storage capacity of approximately 6 GW (mostly pumped hydro), underscoring the need for robust policy and regulatory support to accelerate storage deployment at this scale.

The modeling study takes into account the 27 GW of new coal capacity currently under construction, slated for commissioning by 2030. However, apart from this under-construction capacity, no additional coal capacity is found to be cost-effective by 2030. The total cost-effective coal capacity by 2030 is projected to be 242 GW.

The non-fossil share of total electricity generation is expected to more than double between 2023 and 2030, increasing from 26% in 2023 (including large hydro and nuclear) to 58% by 2030, and reaching 60% by 2032. Despite nearly doubling electricity demand, thermal generation remains relatively stable, ranging between 950-1,000 TWh per year (ex-bus). In contrast, renewable energy generation (excluding large hydro) is projected to increase substantially, rising from 210 TWh in 2023 (13% of total generation) to 1,025 TWh by 2030 (44% of total generation), and further to 1,195 TWh by 2032 (47% of total generation).

The average cost of power generation, factoring in both fixed and variable costs of existing and new capacity, is projected to decline slightly in real terms, from the historical level of Rs. 3.85/kWh to Rs 3.82/kWh by 2030 and further to Rs 3.78/kWh by 2032, despite significant clean energy expansion.

Remarkably, even without Renewable Purchase Obligations (RPO) or the national storage target, the least-cost resource mix for FY 2030 still consists of 504 GW of non-fossil capacity. This includes 303 GW of solar, 105 GW of onshore wind, 7 GW of offshore wind, 15 GW of biomass and small hydro, and 59 GW of large hydro. Additionally, the economical energy storage requirement is found to be approximately 51 GW, comprising 42 GW of battery storage and 9 GW of pumped hydro. By 2032, cost-effective non-fossil capacity is projected to increase to 590 GW, including 372 GW of solar, 105 GW of onshore wind, and 16 GW of offshore wind, supported by 86 GW of storage. Optimal coal capacity by 2030 is found to be 244 GW, implying only 2 GW of additional coal capacity beyond the 27 GW already under construction. By 2030, the average cost of generation is expected to reduce slightly by 2% in real terms, to Rs. 3.76/kWh

.

Table ES-1 summarizes the key scenario results.

Table 1. Installed capacities, average costs of generation, and share of non-fossil resources in total electricity generation (2023 and 2030)

Property | Technology | Actual (2023) | Reference Case (2030) | No RPO and Storage Targets (2030) | High Battery Cost (2030) | Low PHS Cost (2030) | Restricted Storage Deployment (2030) |

Installed Capacity (GW) | Coal | 213 | 242 | 244 | 242 | 242 | 270 |

Natural gas | 25 | 25 | 25 | 25 | 25 | 25 | |

Nuclear | 7 | 14 | 14 | 14 | 14 | 14 | |

Hydro (incl Small Hydro) | 50 | 64 | 64 | 64 | 64 | 64 | |

Wind | 44 | 126 | 112 | 127 | 126 | 127 | |

Solar | 66 | 315 | 303 | 315 | 316 | 311 | |

Biomass | 10 | 10 | 10 | 10 | 10 | 10 | |

BESS | 0 | 51 | 41 | 41 | 42 | 10 | |

Pumped Hydro | 5 | 9 | 9 | 18 | 17 | 11 | |

Total | 420 | 856 | 823 | 856 | 856 | 842 | |

Average Cost of Generation (Rs/kWh) | 3.85* | 3.82 | 3.81 | 3.86 | 3.81 | 3.92 | |

Share of non-fossil resources in total electricity generation (%) | 26% | 58% | 55% | 58% | 58% | 57% | |

* Model estimate

By 2030, a total of 61 GW/218 GWh of energy storage is projected to be cost-effective to support 500 GW of clean power capacity. This requirement is expected to grow to 96 GW/362 GWh by 2032 (as illustrated in Figure 2).